Ethereum Defi: The New Price Fuel?

As tokens once more rise seemingly out of nothing to gain a billion dollars market cap in days, the potential resemblance to the ICO boom hasn’t escaped many.

Not least because these are in some ways public offerings of ownership of public code, but this time it is code that has actually been built and it has users.

That limits the number of potential participants as you need a product first to then sell the rights to participate over how to run the code business.

That acts as a sort of quality scanner, but there are still plenty of low hanging fruits in the decentralized finance space to build new products as well as to develop on the synergy of dapps that have already been built.

It’s not clear however why all this should necessarily reflect on the price of ethereum itself. Positively that is, or even negatively.

The 2017 boom has been attributed to Initial Coin Offerings (ICOs) by many, with the argument somewhat simple.

A lot of promises were being made to built innovative projects, a global audience hungry for new investment opportunities could not get enough of them with many ICOs ending in seconds, and most crucially almost all these ICO tokens were priced in eth.

You therefore needed eth first. And what is also very important if not crucial, is that once this eth was sent over to the dappers for the tokens, the dappers generally kept the eth instead of fiating it.

Therefore not only was there new demand for these new investment opportunities, but total supply also practically fell by about 10%.

Defi is different because you’re not giving eth for these tokens. Instead the tokens are given out for free to the users of the dapp. Once these tokens have a market, it’s then the usual supply and demand and in this case not just in return for eth, but also btc or usdt or whatever else depending on the exchange.

In addition, the users of the dapp don’t have to be ethereans specifically. They can be bitcoiners with their wbtc, or they can be primarily token holders.

However, if we look at this more holistically, defi like icos can lead to both an increase in demand and a practical contraction in supply.

If we look at cryptos in general instead of just eth, you’d think more people than usual would now convert their fiat because there’s more things they can do.

Except there’s usdt, but that is backed by cryptos as well as dollars. Coinbase’s version of usdt is just dollar per dollar, but interest rates in defi are usually set algorithmically depending on how many want to lend or borrow.

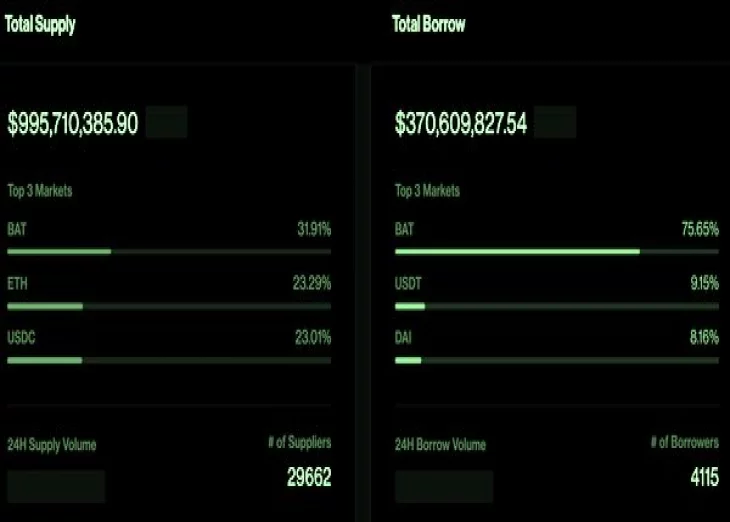

So usdc, for example, is currently attracting an interest rate of 0.13% on Compound. BAT, on the other hand, is at more than 13%.

All these fluctuations create some barrier to entry, but the ICO tokens were also bought by bots mainly. So here too there are dapps where you deposit your crypto and then let the bots manage it to gain the highest amount of profit.

All these eth and tokens that are deposited in these dapps are then practically removed from circulation.

They may be converted for other tokens or even usdt, but they stay within the crypto system. They don’t go back to fiat because fiat interest rates are 0%.

So there’s the potential here to have the same combination of increased demand and practically contracting total supply, but this time eth will share both with other tokens.

Copyrights Trustnodes.com

Article comments